All Categories

Featured

Table of Contents

They generally give a quantity of coverage for much less than long-term sorts of life insurance policy. Like any type of policy, term life insurance has advantages and downsides depending upon what will function best for you. The benefits of term life include affordability and the capacity to tailor your term size and protection quantity based on your needs.

Relying on the sort of policy, term life can use set premiums for the entire term or life insurance policy on degree terms. The survivor benefit can be taken care of as well. Because it's an affordable life insurance policy product and the repayments can remain the very same, term life insurance coverage policies are prominent with youngsters just beginning, family members and people who want protection for a specific time period.

Outstanding Guaranteed Issue Term Life Insurance

Fees show policies in the Preferred Plus Price Course issues by American General 5 Stars My representative was extremely well-informed and useful in the process. July 13, 2023 5 Stars I was pleased that all my demands were satisfied promptly and properly by all the representatives I talked to.

All paperwork was electronically finished with accessibility to downloading and install for personal data maintenance. June 19, 2023 The endorsements/testimonials presented ought to not be construed as a recommendation to purchase, or an indicator of the worth of any services or product. The testimonies are actual Corebridge Direct consumers who are not affiliated with Corebridge Direct and were not given compensation.

1 Life Insurance Coverage Stats, Information And Sector Trends 2024. 2 Cost of insurance coverage prices are figured out utilizing techniques that vary by company. These rates can differ and will generally boost with age. Prices for active staff members may be various than those offered to terminated or retired workers. It is very important to look at all factors when reviewing the total competitiveness of prices and the worth of life insurance protection.

Comprehensive Term Life Insurance For Couples

Like a lot of team insurance policy plans, insurance plans provided by MetLife contain certain exclusions, exemptions, waiting durations, reductions, constraints and terms for maintaining them in force (what is level term life insurance). Please call your benefits administrator or MetLife for costs and total details.

For the most component, there are two types of life insurance plans - either term or irreversible strategies or some mix of both. Life insurance firms supply various forms of term plans and traditional life plans as well as "passion sensitive" items which have ended up being extra widespread since the 1980's.

Term insurance coverage supplies security for a specified period of time. This period can be as brief as one year or provide protection for a details variety of years such as 5, 10, twenty years or to a defined age such as 80 or in many cases approximately the earliest age in the life insurance policy mortality tables.

Premium Level Term Life Insurance

Currently term insurance policy prices are really competitive and amongst the most affordable traditionally experienced. It ought to be kept in mind that it is a widely held belief that term insurance is the least costly pure life insurance policy protection offered. One requires to assess the plan terms thoroughly to make a decision which term life choices appropriate to meet your particular scenarios.

With each new term the costs is boosted. The right to restore the plan without proof of insurability is an important benefit to you. Or else, the threat you take is that your health and wellness may weaken and you may be not able to obtain a plan at the same rates or also whatsoever, leaving you and your beneficiaries without insurance coverage.

You must exercise this choice during the conversion period. The length of the conversion period will vary relying on the kind of term policy purchased. If you transform within the prescribed period, you are not required to offer any kind of info concerning your wellness. The premium rate you pay on conversion is typically based on your "present achieved age", which is your age on the conversion day.

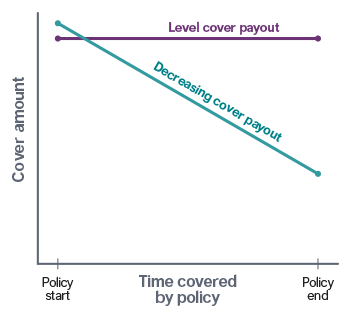

Under a level term plan the face amount of the policy remains the same for the entire period. Commonly such policies are sold as mortgage security with the amount of insurance reducing as the balance of the home mortgage decreases.

Commonly, insurance companies have actually not had the right to alter premiums after the plan is offered (what is direct term life insurance). Considering that such plans might proceed for years, insurance firms should make use of conventional death, passion and expense rate price quotes in the costs computation. Flexible premium insurance coverage, nevertheless, enables insurance firms to offer insurance policy at reduced "existing" premiums based upon much less conservative presumptions with the right to change these costs in the future

High-Quality Group Term Life Insurance Tax

While term insurance is developed to give protection for a specified period, permanent insurance coverage is designed to offer protection for your whole life time. To keep the costs rate degree, the costs at the more youthful ages exceeds the real cost of defense. This added premium constructs a reserve (cash value) which aids pay for the policy in later years as the price of protection increases above the premium.

Under some policies, costs are needed to be paid for an established number of years. Under other policies, costs are paid throughout the policyholder's life time. The insurance provider invests the excess premium bucks This sort of policy, which is often called cash money value life insurance, generates a cost savings element. Money values are vital to a long-term life insurance coverage plan.

Top The Combination Of Whole Life And Term Insurance Is Referred To As A Family Income Policy

Occasionally, there is no correlation between the size of the money worth and the costs paid. It is the cash money worth of the policy that can be accessed while the policyholder lives. The Commissioners 1980 Requirement Ordinary Mortality (CSO) is the existing table made use of in calculating minimum nonforfeiture values and plan gets for regular life insurance policy policies.

There are 2 basic groups of long-term insurance policy, typical and interest-sensitive, each with a number of variations. Typical whole life plans are based upon long-term price quotes of expenditure, interest and death (term life insurance with accelerated death benefit).

If these estimates alter in later years, the business will adjust the premium appropriately yet never over the maximum assured premium stated in the plan. An economatic entire life plan attends to a basic amount of taking part entire life insurance policy with an added supplemental insurance coverage supplied through making use of rewards.

Due to the fact that the premiums are paid over a much shorter span of time, the premium settlements will be more than under the entire life plan. Single premium whole life is minimal payment life where one huge exceptional repayment is made. The plan is fully paid up and no additional costs are needed.

{kind=link}

Latest Posts

Omaha Burial Insurance

Memorial Service Life Insurance Company

Burial Life Insurance Seniors